*Adding up* with Blackstone

BCRED's inCREDible fee misalignment

Last week, Blackstone’s Jon Gray spoke at a meeting with “top financial advisors.” Whether “top” referred to fee generation, or client returns, we are not sure. We think, probably, not both.

Gray walked through a hypothetical “doom scenario” in which private credit encounters very high--worse than the GFC-- losses and concluded that the financial media (and perhaps the market) seem to have it wrong.

The Blackstone description of the video:

“Gray explains why the math doesn’t add up on some of the predictions around private credit.”

In Gray’s ‘doom’ scenario, BCRED’s returns would stay nicely positive in a crisis.

We’re not sure that is a high enough performance standard, but that’s just us.

If the current weakness in private credit is unmerited, then similar publicly-traded debt vehicles, which currently trade at large discounts to NAV, should instead be trading at NAV. Just like BCRED.

But they aren’t. This is the math that doesn’t “add up.” And aside from the more friendly math, you can buy publicly traded debt BDCs today and sell them tomorrow, if that’s your jam.

While it would suit Blackstone if leading advisors ignored this, the advisors wouldn’t be doing their job if they did, would they? Kind of reminds you of BREIT in 2022, doesn’t it?

Unfortunately for end-investors, the decisions of advisors, even (especially?) top advisors, can be distorted by financial incentives.

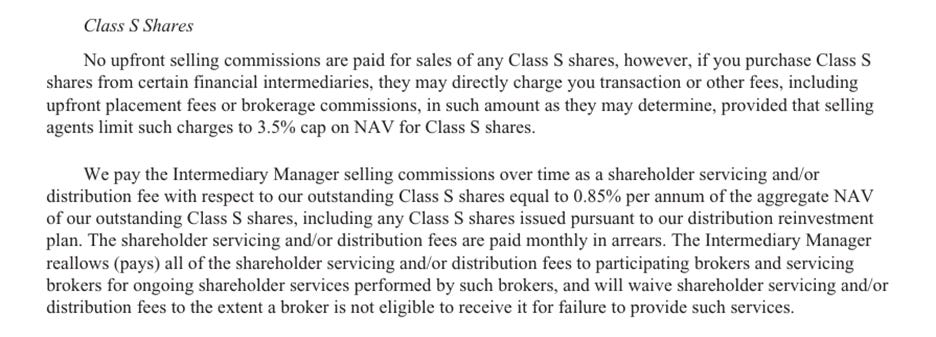

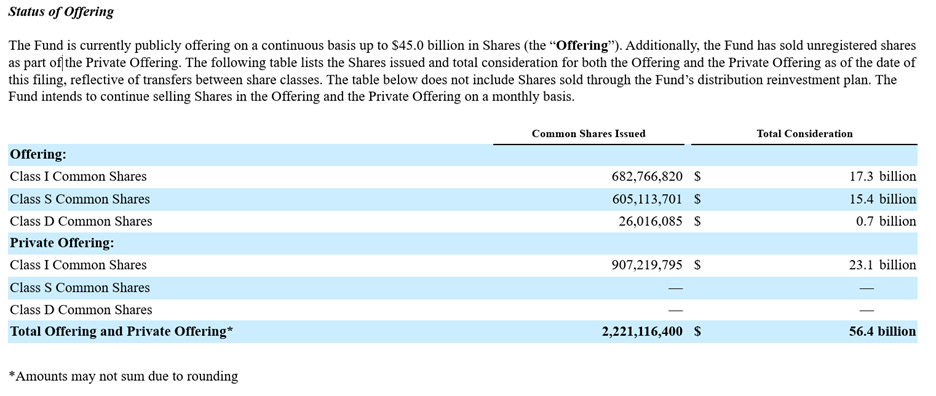

Take the revenue that flows to leading advisors from having put their clients in BCRED in the first place. Based on BCRED’s March 20 8-K filing, that would be $131 million per year for the Class S shares. These fees are in addition to BCRED’s management and incentive fees.

Blackstone sees the problem (of broker-dealers getting religion) clearly: From page 1,448 (!) of BCRED’s 10-K:

They definitely exist lol

Speaking of adding up

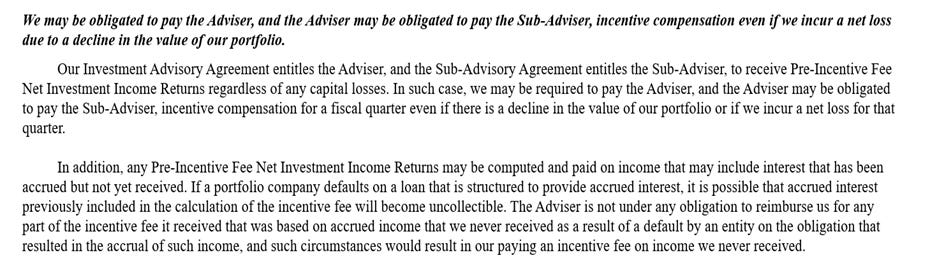

You know what might not be affected much at all in the doom scenario described by Gray? BCRED’s own incentive fees.

BRED is widely understood to have a 5% hurdle rate before incentive fees can be paid. Unhelpfully for investors, this hurdle applies only to income, not to capital gains. In Gray’s ‘doom’ scenario, the BCRED fee machine would just power through. But hey, good for BX shareholders, right?

And in case you were wondering, PIK interest counts as income.

Good luck, top advisers!

Jon Gray on Instagram:

BCRED 8-K Filing, March 20:

BCRED 10-K, March 14: