Cliffwater: Losing Intellectual Dignity

...for sure. Keeping AUM? We'll see.

Cliffwater:

1. Touts strong private debt performance after periods of weak publicly-traded debt BDC performance, but:

2. Disrespects investors: omits the same data for publicly-traded BDCs, which (surprise!) performed far better.

Cliffwater and its (conflicted?) defenders, along with other private debt fund managers (ex: Blackstone), argue that private debt owners should remain invested.

The frequent vibe: investors need to be a bit more brave. That changing one’s mind and redeeming reflects a certain short-termism. Betrayal, even.

This messaging often works: we all want to be brave, loyal, long-term investors, right?

But long-term, brave investors can—and should—remain open to clear opportunities.

Active investors-by definition-choose not to own everything that they could.

If something they don’t own declines in price, while similar things they do own maintain value, shouldn’t that feel like an opportunity? If buying the cheap thing and selling the expensive one doesn’t sound like the proverbial ‘fat pitch’, what would?

Delivering Transparency….

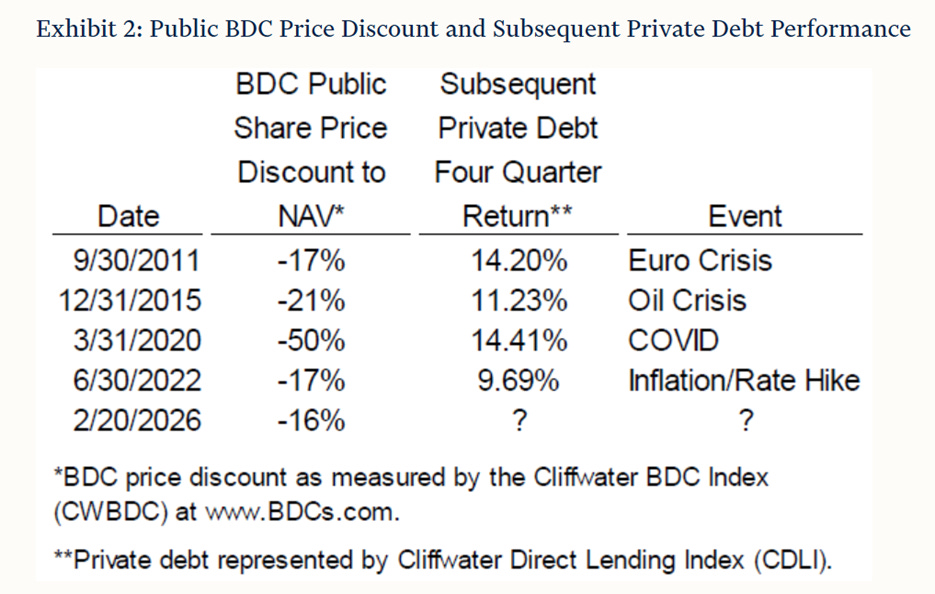

Cliffwater’s CLDI index measures the performance of direct loans, both exchange-traded and unlisted. From last month’s report entitled “New Private Credit Data Contradicts the Recent Risk Narrative:”

In addition to providing an index, Cliffwater also manages (lately quite a lot of) money. As an example, the Cliffwater Corporate Lending Fund (CCLFX) is similar to a private debt BDC in its investment style and structure.

CCLFX and other private funds do not trade on exchanges. When you want your money back, you can do it only at specific intervals. And when you do, the price you’ll pay/get is Net Asset Value, or the value ascribed to the fund’s holdings by said managers.

Meanwhile, publicly traded debt BDCs own similar stuff. But the market decides on any given day what they are worth.

Lately the price of publicly traded debt BDCs has fluctuated…downward. The prices of private funds? Much less so.

Cliffwater’s report acknowledges this dynamic, as well the fact that it reflects concerns about quality of the loan-investments in these BDCs.

So far, so good.

…Into an otherwise opaque market?

Cliffwater’s report then highlights that following past periods of weakness, subsequent private debt performance (which, again, do NOT trade on public exchanges) was strong, with the average return of 12.38%:

Cliffwater presents the below table:

….What the hell?

Are Cliffwater serious? Where is the column with the subsequent returns for public BDCs?

Helpfully, Cliffwater provides this data (free!). We downloaded it.

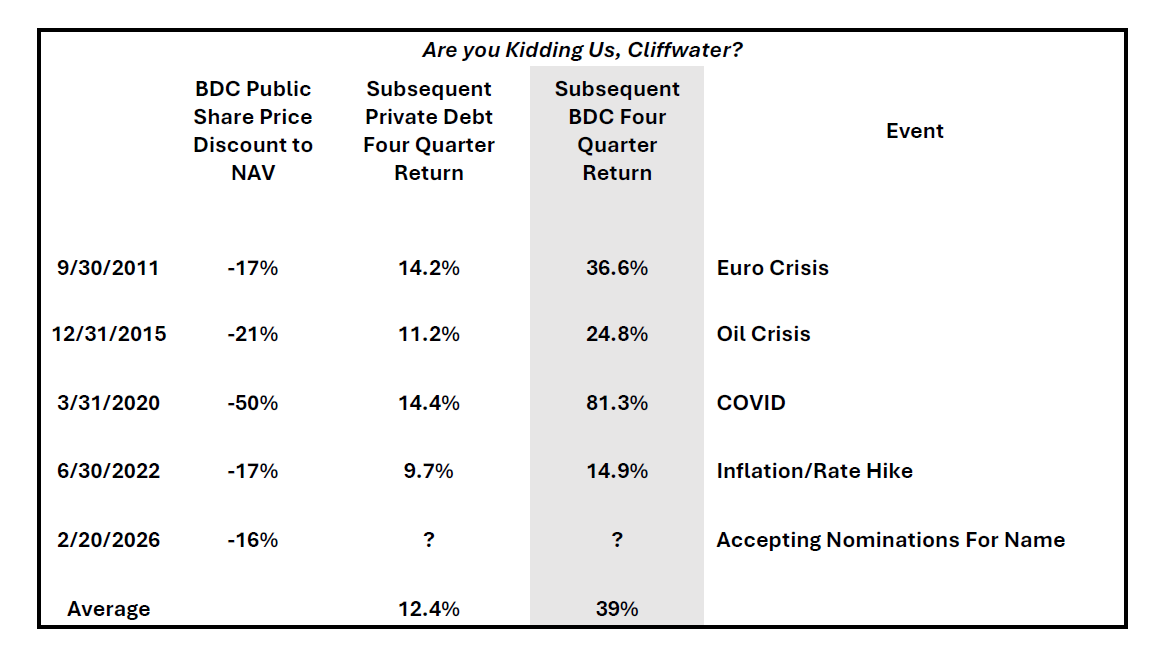

The AltView spent 5 minutes creating the below cool excel table that to our mind properly removes opacity.

Publicly traded BDCs (highlighted in grey) handily outperformed private debt each of the four times this has happened in the past.

The average return, touted by Cliffwater, was 12.39% for private debt.

For the public BDCs, the average return was…wait for it… 39%.

Actually 39.4%. We rounded down to be more sporting.

This information:

1. Does not surprise, sadly

2. Supports doing the opposite of what Cliffwater suggests; getting out of private debt products, not staying in them.

Most important; Cliffwater’s dodgy presentation suggests that they favor their own wealth at the expense of their intellectual dignity and their investors’ wealth.

Not a good look if you ask us.

NOT INVESTMENT ADVICE

Resources:

Cliffwater “Risk-Narrative” Report

https://cliffwater.com/ResourceArticle/new-private-credit-data-contradicts-the-recent-risk-narrative?docId=30429

BDC Database:

Larry Swedroe’s (conflicted?)

Substack on Cliffwater:

Brian’s Hat, full episode (you’re welcome!)

As for the name for this event, maybe “Media manufactured SaaSpocalypse AI hysteria + operation [not so] epic fury”

The private BDC-ers have tons of fee incentive to suggest an investor not redeem. But isn’t the obvious “trade” to sell/redeem the non-public BDC at NAV, buy the public BDC at a discount to NAV, and pocket the difference between non-public NAV and the public discount to NAV?

Non-public OBDC II has some 90%+ overlap with public OBDC. The real mystery is why OWL was shocked that OBDC II investors were pissed they were getting liquidity via a NAV-for-NAV combination that would give them an immediate 30% paper loss.