Today we won’t focus on our (evidence-based) belief that Alts in 401k plans aren’t worth the bother. Instead, we will show how Alts fees might solve industry problems, as a way of explaining the industry’s unbridled enthusiasm for them.

Perhaps the most coveted spot in the 401(k) world is Target Date Funds, or TDFs. These are the simple, set-it-and-forget-it-funds that typically have a simple mix of stocks and bonds. The asset mix changes as the employee ages: young employees are mostly invested in stocks; over time, the asset allocation gets more conservative.

The TDF market is coveted because it is:

1. Big ($3.5 trillion in 2023, almost 4x that of 2014) and

2. Has healthy inflows of money each year. (1)

But the pricing trend is bad for the industry, as the above chart shows. If only there were a way to fix this….

Enter Alts.

Magic! The expense ratio nearly doubles.

The Alternative view thinks these charts explain a lot of recent industry acquisitions and tie-ups at (for example), Capital Group, State Street, Franklin Resources, and Blackrock.

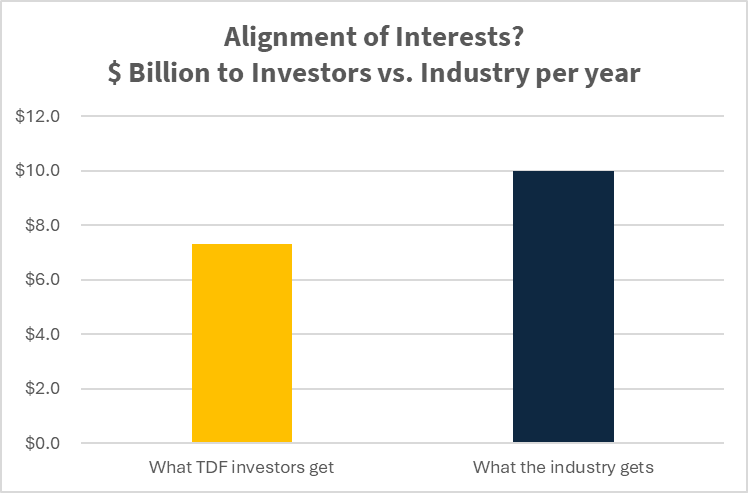

A dollar for me, 73 cents for you

Georgetown research (2) we discussed last week celebrates the (hypothetical, of course 😊) incremental dollars earned per year by 401(k) Target Date Fund investors, were they all to allocate to alternatives (instead of, say, boring stocks).

Using the Georgetown approach, we can calculate that replacing 10% of stocks with private equity (one of the options in the research) would result in $7.3 billion incremental dollars per year to those lucky TDF investors. (3)

Here at The Alt View we wondered: What would the industry get?Now, consider the same figures, but with a portfolio allocated 10% to private equity in 2024 (at a conservative 3% expense ratio for this allocation).

The answer: $10 billion.Every year. The above again assumes a (super-conservative, we know!) 3% fee on private equity investments. Call us crazy but to us the chart looks lopsided, and in the wrong direction.

And what if some of those PE investors were not lucky? If their results, for example, only matched those of public equities (the return of which can basically be gotten for free), would their fees on their private equity investments be, like, zero? Alas, this is not how things work.

Making this dynamic particularly troublesome is the fact that LOTS of private equity funds—and a majority of funds of funds (the likely vehicle for 401(k) plans) have underperformed equity markets (4). Underperformance with alts even occurred 20% of the time in the (rosy, in our view) Georgetown private equity scenarios. That would never happen to us, would it?

Channel David Swenson (or maybe Vinnie Daniel)

The Alternative View’s clear advice to Fiduciaries: When interacting with Alternatives Sellers, or those that advocate investing in Alternatives, Heed the words of David Swenson:

“By evaluating each participant involved in investment activities with a skeptical attitude, fiduciaries increase the likelihood of avoiding or mitigating the most serious principal-agent conflicts.”(5)

Or, Alternatively, adopt the mindset of Vinnie Daniel of Big Short fame, who regularly asked those that came to his team with investment ideas:

“Tell me how are you are going to f***k us.”

Incentives affect behavior. Could it be that the Alts acquisition binge, and in turn, the Alts-in-401(k)s pitch, reflects a kind of desperation among asset management firms?

Selling Alts is clearly good for them.

Is buying Alts good for you? Be Careful Out There, Fiduciaries!

3) This approach uses Using the total TDF market size of $3.3 trillion and an assumed amount of Alts outperformance (.22 bps per annum) for a portfolio with a 10% in Private equity allocation (instead of public equity).