State Street's Math Challenges, feat. Apollo

Living(-)

Our favorite Succession episode was Living+ (Season 4).

New Co-CEO Kendall Roy, fending off a hostile takeover of his family’s company, Waystar Royco, is desperate to juice the company’s stock price in an effort to keep Scandinavian suitors at bay.

Over the vehement objections of Waystar Royco’s finance execs (CFOs are fiduciaries, right?), Roy promotes absurd earnings projections for a fledgling division called Living +. He uses his propaganda skills to wow the analysts gathered in LA, magically morphing the concept from a gated community to a life-extension service.

To top it off, Kendall orders production of a deepfake video in which his recently-deceased dad promises that Living+ could support a doubling of the company’s Parks and Cruises division.

And guess what? It works! At least on the day, anyway.

It’s a great segue to today’s Alt’s in 401(k)s offering, State Street’s Target Retirement IndexPlus Strategies.

In preview: we think State Street may have got their arithmetic operation wrong. And their partner’s (Apollo) product keeps dialing back expectations.

______________________________________________________________

State Street, asset management behemoth with $4.8 trillion in AUM, is keen to get Alts in DC retirement plans. The company already has nearly a quarter trillion in target date fund assets.

The “Plus” offering, launched in April of 2025, consists of simple, investor friendly passive stock and bond investments coupled with an, err, complex, expensive, illiquid allocation to Apollo Aligned Alternatives “AAA” -Apollo’s flagship fund.

Aside from the potential for excess return (compared to what, they don’t say, but we’d like to think it is public equities), IndexPlus also promises transparency, sophistication, and diversification.

State Street did its research before settling on AAA:

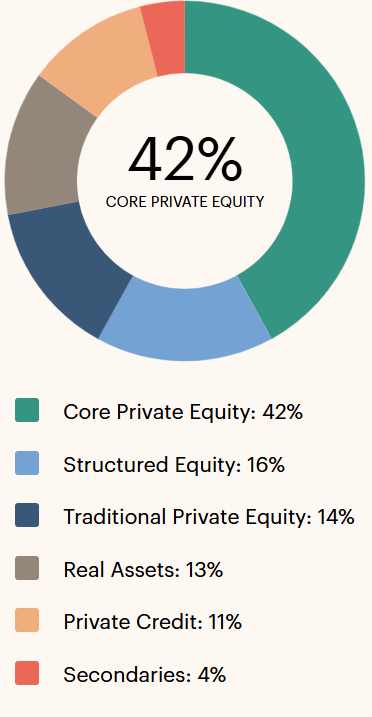

What’s in AAA?

As AAA is available as a standalone product, interested investors can undertake their own due diligence. AAA’s allocation:

By our simple math and stubborn fiduciary logic (i.e. getting compensated for illiquidity and leverage), we reckon this strategy should need to offer prospective returns of at least 2% over public equities to get us interested.

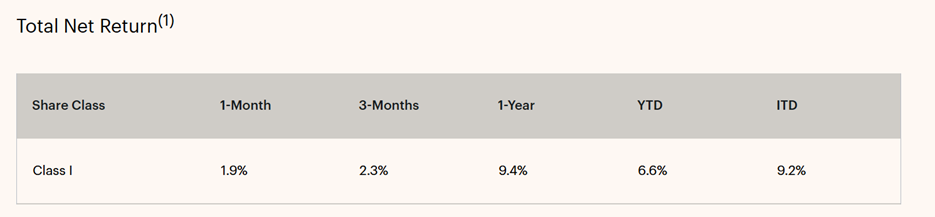

So have AAA’s historical returns been worth the bother?

Total annualized returns for the period from June 30, 2023, to September 30, 2025 (puzzlingly, this is the most recent update available for AAA), are:

S&P 500: 21.5% (SPY)

MSCI ACWI: 19.5% (ACWI)

S&P 600 Small Cap 10.1% (SPSM)

AAA 9.2%

Behold, Living Minus!

We readily concede that two+ years is a short period of time. Still, if the AAA fiduciary-investor is expecting better than equity returns from AAA then this strategy will need heroic performance prospectively to restore faith. Even against the small cap index, things don’t look good.

Illustrative Returns…

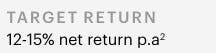

While the formal AAA product was launched only recently, there is information out in the ether regarding Apollo’s marketing and targeted performance for the strategy. Expectations have evolved.

From a 2024 communication:

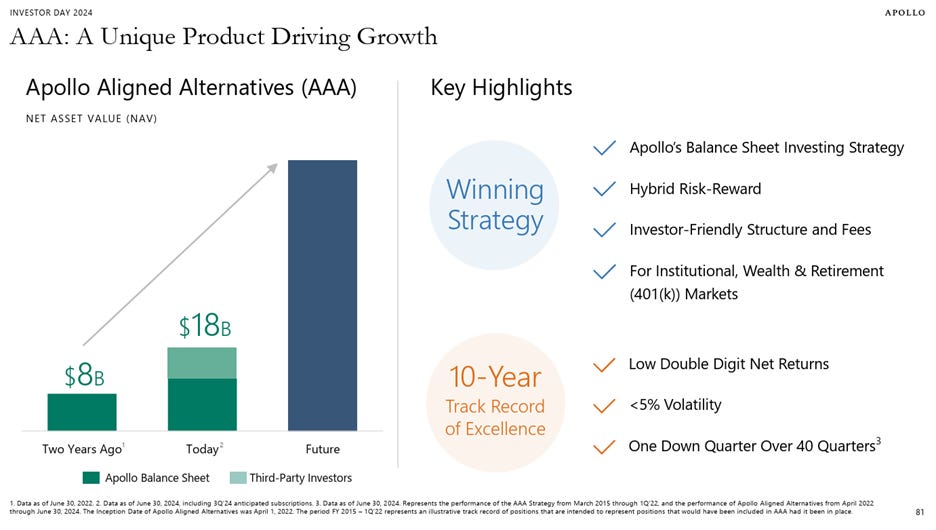

At Apollo’s 2024 investor day, with the addition of real-life returns to the track record, the vibe was more muted (‘low double-digit’):

The investor day slide also highlights a 10-year “track record of excellence”.

Let’s zoom in on that footnote:

AAA’s 10-Year Track Record of Excellence, which Apollo calls “illustrative” benefits from several years of results that we might call invented. The results reflect strategies that Apollo decided to include in AAA but were not actually realized by any investor-client. Other Apollo documents show that they exclude stuff like Oil and Gas investments and ‘Discontinued Strategies’ (performance was great, we just decided to shut it down….).

Anyway, If AAA’s actual investment results have lagged its old targets (and equity markets broadly), we can see that the asset gathering strategy is working great. AAA has $24.2 billion in AUM as of September 2025.

Yet return expectations keep getting managed down. Below is from AAA’s latest fact sheet:

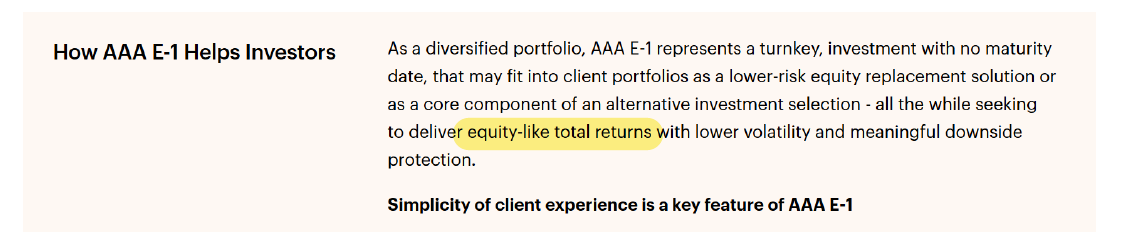

“Equity like?” No illiquidity premium, Apollo?

And State Street: are you still on board with this?

And note the pivot: Apollo is now focusing on risk, suggesting that levered, illiquid private equities are a “lower risk equity replacement solution” compared with publicly traded stuff.

Curious to know more, we reached out to State Street corporate comms. We also tried to contact the author of State Street’s stuff on Index Plus. We reached out to Apollo comms. We did not get a response.

Hey! That’s Unfair

A knock on this argument: it’s only a couple years. Fair enough.

It’s also true that the State Street product only came into existence in April of 2025, so did not suffer from all of AAA’s weak relative performance.

But had State Street invested in ‘illustrative’ AAA since its hypothetical beginning, the juice would still not have justified the squeeze in our view.

One possibility: maybe State Street takes a more optimistic view of AAA’s future return prospects than its rough early start.

Another possibility is that State Street hoped that AAA’s returns would be notably better out of the gate (our suspicion is that the TDF strategy has only a small amount of AUM) and that State Street hoped to later market based on its track record.

We’d like to ask State Street about these things, and also how State Street considered Apollo’s illustrative returns in its due diligence.

We’d also want to know how much more the Index Plus strategy adds to State Street’s fees vs. its simple, flexible, liquid and cheap iteration. After all, if IndexPlus’ investors pay standard fees for AAA, then the cost of IndexPlus vs. a passive State Street fund could easily go up 5x or more. IndexPlus, indeed!

State Street’s IndexPlus:

State Street’s “Private Markets in Target Date Funds” why now?

https://www.ssga.com/us/en/intermediary/insights/private-markets-in-target-date-funds

State Street’s April 2025 press release:

https://newsroom.statestreet.com/press-releases/press-release-details/2025/State-Street-Global-Advisors-Announces-State-Street-Target-Retirement-IndexPlus-Providing-Defined-Contribution-Investors-Access-to-Both-Public-and-Private-Markets-Exposures/default.aspx

Apollo Aligned Alternatives Fact Sheet

https://www.apollo.com/wealth/strategies/products/apollo-aligned-alternatives-e1

AAA fact sheet from December 2024

https://www.fidante.com/au/APOL-FF-AAA.pdf

Apollo 2024 Investor Day Slides

https://ir.apollo.com/news-events/investor-day-2024

Pensions & Investments re: State Street TDF

https://www.pionline.com/defined-contribution/ssga-and-apollo-launch-target-date-funds-offering-plan-participants-90-10-mix/

Really hard not to look at most of PE as just asset gatherers earning fees on “low vol” investments they never accurately mark to market bc if they did it would lower their hefty fees. What Apollo are doing with Athene (dumping their crappy PC investments into their insurance arm) is highly questionable too. Quasi-ponzi schemes at this point yet too big to fail now

Thanks for this write-up! A few comments:

(A) I love the abbreviation "AAA" (the highest rating!).

(B) I understand that this fund will be included at 10% of the SSgA target date fund across the entire "glide path". This seems antithetical to the notion of a glide path, which ordinarily reduces risk as participants approach retirement. This means that for those approaching, or in, retirement, this fund is a larger percentage of the portfolio's risky asset component. For example, if the glide path calls for only 20% risky assets at an older age, this is half.

(C) On a webcast rollout, I submitted the question as to how they set the allocation among various classes of private assets, and they basically said "opportunistically" (your opportunity or theirs?). No fixed strategy. It appears to be whatever Apollo has on its balance sheet at the time. They market that Apollo owns most of the fund (or Athene, their insurer, does, at least) as a plus, because it means they believe in it. To me, that sounded like a Chevrolet dealer telling you "look at all the Chevy's on our lot -- we really believe in them" (or haven't been able to unload them). Also, on the webcast, they addressed liquidity concerns by noting that the other 90% of the assets in the target date fund are liquid - so if the target date fund experiences a lot of exits, those left will end up with a higher percentage of their portfolio in this.

(D) This fund, I understand, will be housed in a "collective investment trust," a special type of investment vehicle for US tax-qualified retirement plans only intended to be mutual fund-like except with less required disclosure. So if you're expecting lots of transparency, I wouldn't hold my breath.

Of course, I could be wrong, but this looks to me like an outlet for Apollo to reduce inventory and collect some nice fees on their main balance sheet portfolio on which they've been collecting nothing? It reminds me of the loan portfolio that Apollo's ARI REIT, trading at 77% of book, "sold" to Athene (but they're the same...) for 99.7% of book (see https://giftarticle.ft.com/giftarticle/actions/redeem/b6e8386f-1a67-4d4e-99e6-dc0d751e6f3b).

It will be interesting to see whether this or similar products gain traction with employers.