Time to pay the fiddler

Private Equity challenges in four charts

Weird Science, 1985. Truth: I never really watched it but my college roomates constantly quoted it.

Recent attention has been focused on Private Debt troubles, sometimes linked to borrowings of tech (often software) related companies.

The stated maturity of private debt financing is typically 5-7 years.

It’s time to pay the fiddler. Hence the recent commotion, it seems.

If Private Debt-financed software companies might suffer from AI-related threats, private equity investments in the same stuff is going to be in much worse shape.

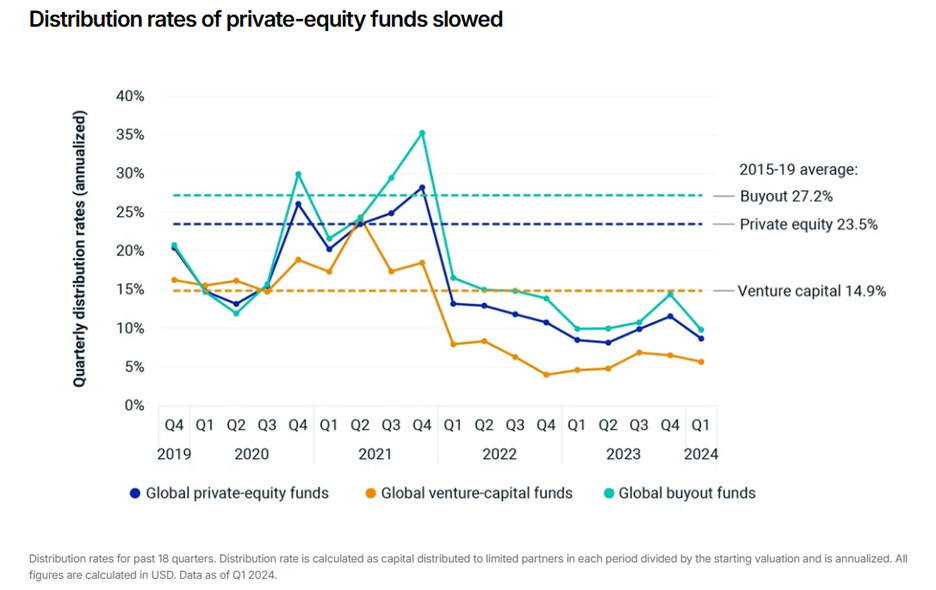

Remember COVID? It sucked, but refinancing your mortgage was a nice silver lining. Markets boomed. In 2020 and 2021, it was a real challenge for institutional investors to keep asset allocations high for PE and for VC; tons of it was getting returned to investors.

Source: MSCI

THIS IS IMPORTANT. If an institution maintained its PE weighting during these years, as most try to do, the stuff it likely owns in its PE tranche was VERY different at year end 2021 vs. the beginning of 2020.

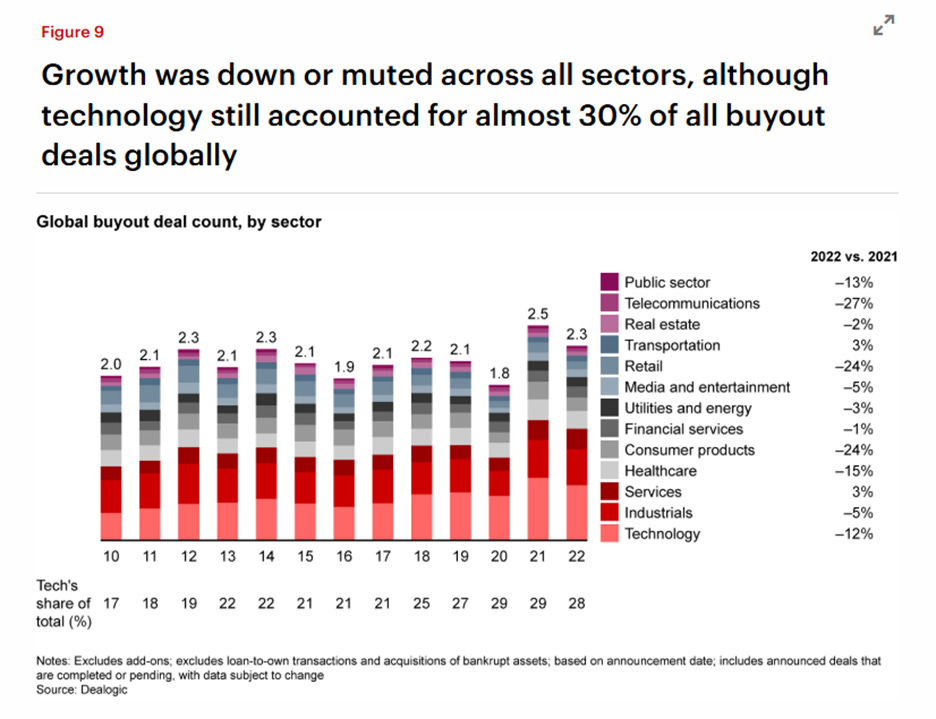

What was being bought? Compared with a decade prior, the share of technology had notably increased (from 19% to 28%). Yes, we know. Tech is not necessarily software. Humor us.

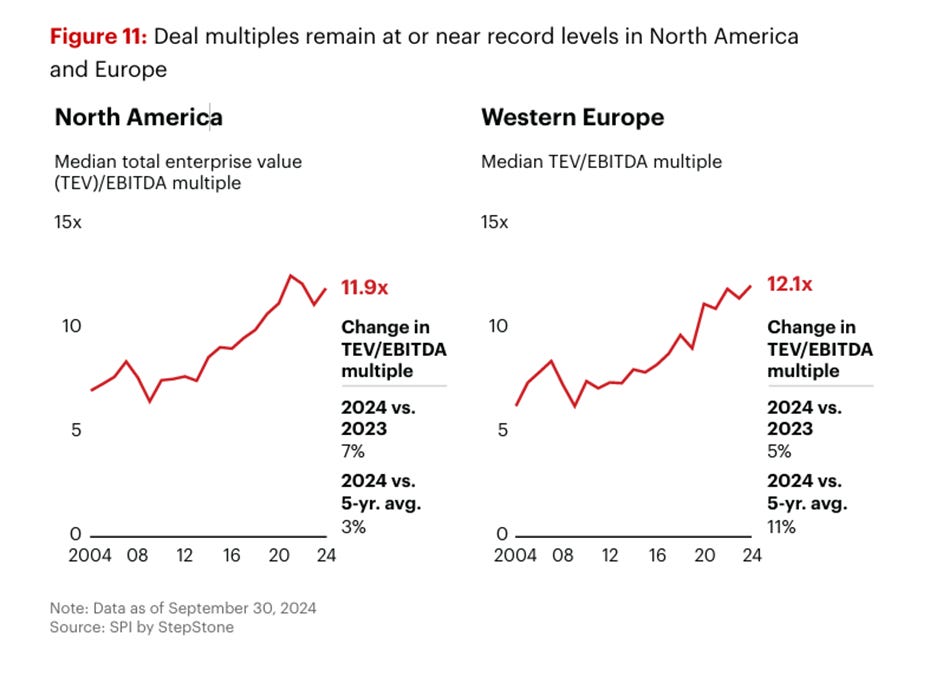

Multiples paid for these businesses were VERY high on average compared with prior years (including prior to the GFC). Look at the charts:

Source: Bain

High multiples were facilitated by very low borrowing costs. Leveraged loans (at floating rates) used to finance the 2020/2021 deals are now much more expensive. (Aside: are we supposed to be excited about PE since EBITDA multiples are 11.9x vs. a peak of say 13x?)

Source: Bain

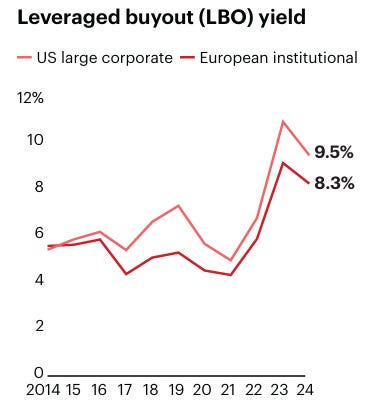

In summary: Multiples in 2020/2021 were VERY high, and finance costs were very low.

Now: financing costs are way higher.

Things were already quite bad for these vintages. To us, the ‘problem’ of low distributions is simply a matter of marks/asking prices being too high.

We have no opinion about the AI threat, but the prospect that some of these businesses might not perform as hoped (independent of finance costs and exit multiple assumptions) feels like a lot of salt in the wound.

Software-focused vintages from those years would seem to be worth perhaps 80% of (GP-reported) NAV at best, using honest, real-time marks.

Here’s an idea for owners of these funds! Instead of doing that, why not sell them to evergreen funds? They’ll pay 90%, then price it at par! Problem solved!

Are we wrong? Tell us!

MSCI:

BAIN:

https://www.bain.com/insights/private-equity-outlook-global-private-equity-report-2023/

You are right - the answer is always related party transactions!

I don't think you are wrong. I would just add that private equity returns are highly asymmetric, and it will be interesting to see who the winners and losers will be from this. My bet is that it's not who you expect - software-focused specialists. It will be software generalists/tourists - of which there were many.